One of the biggest assumptions people make about retirement is this:

“I’ll need the same income every year.”

It sounds logical.

But in reality, retirement spending doesn’t work like that.

In a recent conversation on the Retire Well Podcast, actuary and convenor of the Retirement Income Interest Group or RIIG (https://www.retirementincomegroup.co.nz), Ian Perera, shared what the data tells us about how retirees actually spend, and the results may surprise you.

The Myth of Flat Spending

Many retirement plans, and even online calculators, assume that your spending will stay broadly the same each year, adjusted for inflation.

But according to Ian:

“A lot of the online calculators… make the assumption that you’re going to spend the same amount each year throughout retirement. And the research says that’s actually not how people are likely to spend.”

When we look at real-world data, a very different pattern emerges.

What the Data Shows

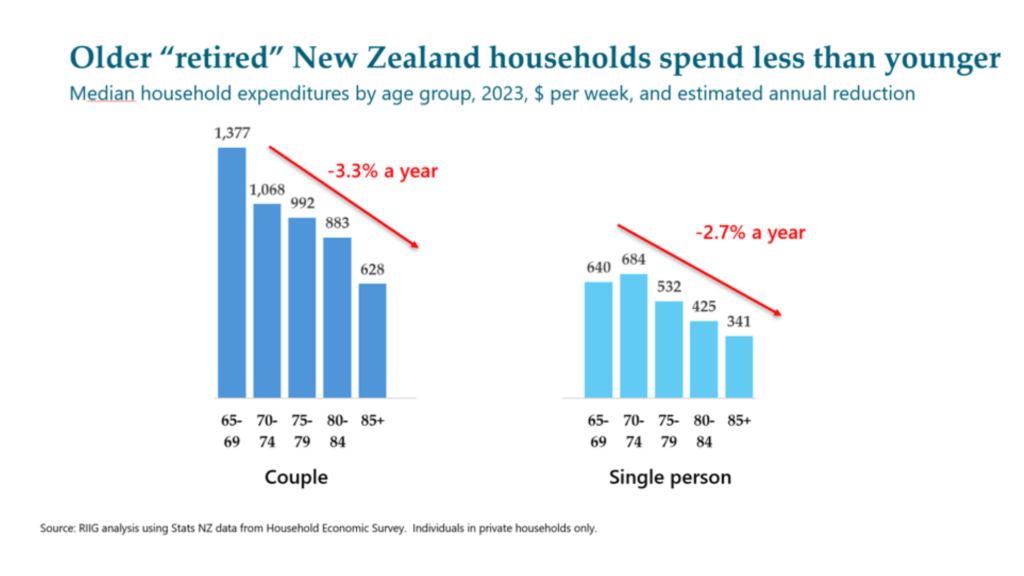

Using data from Statistics New Zealand’s Household Expenditure Survey, Ian and the RIIG analysed how spending changes across retirement.

What they found was remarkably consistent:

Spending tends to decline gradually over time—by around 3% per year as people age.

And importantly:

- This pattern appears both in New Zealand and overseas

- It occurs even among wealthy retirees

- It is not simply due to running out of money

In other words, people don’t spend less because they have to. They spend less because their lifestyle naturally changes.

The Three Phases of Retirement

A helpful way to understand this is through the three stages of retirement:

1. The Go-Go Years

These are the early years of retirement.

You’re active, healthy, and keen to make the most of your freedom.

This is when people tend to:

- Travel more

- Eat out more

- Spend on hobbies and experiences

For many, this is the highest spending period of retirement.

2. The Slow-Go Years

As time goes on, things begin to slow down.

You may:

- Travel less frequently

- Prefer simpler activities

- Spend more time at home

Spending starts to decline—not because you’re cutting back, but because your lifestyle evolves.

3. The No-Go Years

In later life, activity levels reduce further.

Spending typically shifts toward:

- Essentials

- Healthcare

- Support needs

Discretionary spending drops, although certain costs (like care) may increase.

What Actually Drives the Decline in Spending?

One of the most important insights is where the decline comes from.

According to Ian:

“It’s really the discretionary spending which is the one that decreases as you age.”

That means:

- Holidays

- Dining out

- Lifestyle upgrades

These reduce over time.

Meanwhile, essential spending like food, utilities, insurance, and rates, remains relatively stable.

The Role of NZ Super

In New Zealand, NZ Super plays a crucial role in retirement spending. As Ian explains:

“It’s a really important base income… particularly for non-discretionary spending.”

For many retirees, NZ Super helps cover:

- Core living costs

- Essential bills

But it leaves limited room for discretionary spending, especially for renters. This makes personal savings and investment income critical for lifestyle choices.

What Retirees Often Get Wrong

One of the biggest mistakes people make is assuming their spending will stay constant forever.

This can lead to:

1. Over-saving. People delay retirement unnecessarily or underspend in their early years.

2. Missing the “Go-Go Window”. As Ian put it:

“There’s an opportunity… to think about spending a little bit more early in retirement, when you might appreciate it more.”

Your early retirement years are:

- Finite

- Health-dependent

- Often your most active

Delaying spending can mean missing out.

3. Misunderstanding Longevity. At the same time, people often underestimate how long they will live.

Planning to age 75 or 80 may not be enough—many people need to plan into their 90s.

This creates a balancing act:

- Spend enough to enjoy life early

- But not so much that you run out later

A More Practical Way to Plan

Rather than asking:

“What income do I need every year?”

A better question is:

“How will my spending change over time?”

This allows you to:

- Spend more confidently in early retirement

- Adjust spending as your lifestyle evolves

- Align your financial plan with real life

Flexibility Matters More Than Precision

Retirement planning isn’t about finding a single perfect number.

It’s about:

- Understanding your essential vs discretionary spending

- Building flexibility into your plan

- Adapting as life changes

As Ian highlighted, even small adjustments, like changing travel plans, can have a meaningful impact on your overall spending.

Bringing It All Together

Retirement is not a straight line. It’s a dynamic phase of life, where:

- Spending changes

- Priorities shift

- And opportunities evolve

Understanding this can help you:

- Plan more realistically

- Spend more confidently

- And ultimately enjoy your retirement more fully

Where to From Here?

At The Retirement Guys, we help clients build retirement plans that reflect real life, not just spreadsheets.

That means:

- Understanding how your spending may evolve

- Structuring your income to match

- And giving you confidence to enjoy your money

If you’d like to explore how your retirement spending might look, and how to plan for it, we’d be happy to help.